Right of First Refusal (ROFR) is embedded in almost every Shareholders’ Agreement (SHA). It is one of the key investor rights amongst others such as pre-emption, anti-dilution, liquidation preference and so on.

Let’s break down how this actually works, the strategic motives driving it, why it may be regarded as contentious by some, the mechanisms, and the critical scenario that could stall liquidity.

What is ROFR, simply?

Right of First Refusal means: before a shareholder/promoter (depending on the SHA) sells their shares to an outside buyer, they must first offer those shares on the same terms to a specific set of existing investors who have the said right.

Lets understand by an example, where,

A is the promoter

B is the investor who has the right of first refusal , referred to as “ROFR holder”

X is the potential purchaser

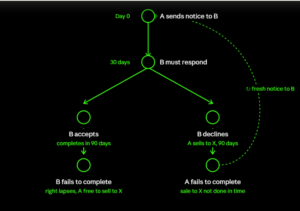

Now, if A has an existing offer to sell a part of his shares to X, at INR100/share, A must first offer them to B on the same terms as offered to X.

Only if B does not exercise its right or waives it off, can A go ahead and sell to X at the same price and terms.

Why do investors want ROFR on promoters’ shares?

a) To get visibility the moment a promoter decides to sell. Without a mandatory notice requirement, a promoter could transfer shares quietly, and investors would only find out after the fact — via a cap table update, or worse, from someone else, much later. A promoter’s exit can signal various things – change in the promoter’s commitment to the company, liquidity for personal reasons, to get some incentive when the company starts doing well (promoters often withdraw very little salary in the initial years).

b) Upside participation. To increase their own stake if there is an upside.

c) To pre-empt an undesirable addition to the cap table. If the promoter sells to an outsider, existing investors have no say over who the new shareholder is — it could be someone with a fundamentally different governance approach, a competitor, or simply a difficult party to work with at the board table going forward.

Why don’t investors want ROFR on their own shares?

It often deters prospective buyers. Secondary buyers — other funds, family offices are reluctant to spend weeks on diligence for a deal that can be matched or blocked by someone else. Many walk away the moment they learn a ROFR exists.

It may also undermine negotiating leverage due to delay in closing the transaction necessitated by following through the ROFR mechanism

If there are 2–3 key investors, how does ROFR actually work? Does every investor in the company get it?

Not automatically. ROFR is a negotiated right, and it’s typically restricted to major or institutional investors — not every shareholder on the cap table.

Whether ROFR holders also have ROFR on each other’s shares depends on the specific agreement — some SHAs restrict it to investor rights over promoter shares only, while others make it mutual among major investors as well.

What if the ROFR holder simply doesn’t exercise the right at all – what happens next?

If investor B, the ROFR holder, receives notice and either declines or doesn’t respond within the notice period, the right lapses for that transaction.

Promoter A now has a clear path: they can proceed to sell to X, the third-party buyer, on the same and no-less-favourable terms than what was offered to B. (This “same terms” condition matters – it stops a seller from lowballing the ROFR holder deliberately, then striking a better side-deal with the outside buyer.)

Agreements also add a time limit on this – A must complete the sale to X within, say, 60–90 days of B’s right lapsing. If A doesn’t sell within that window, the ROFR obligation typically resets, and A has to go through the notice process again before any new sale.

Does tag-along kick in once ROFR is waived?

The typical sequence in a well-drafted SHA is –

- ROFR is offered first. Eligible investors get the chance to buy instead of the outside party.

- If ROFR is waived or lapses, tag-along rights activate for the ROFR holders — they can now choose to sell their proportional share alongside A, to the same buyer, on the same terms.

Often SHAs require B to make an election — i.e., B must choose either to exercise ROFR or reserve the tag-along right for the same transaction.

Why do promoters resist granting ROFR right to investors?

Promoters push back during SHA negotiations to protect their liquidity and strategic freedom. Specifically, a ROFR:

- Restricts Free Transferability: It limits a promoter’s autonomy to freely trade and realize the value of their equity after years of building the company.

- Blocks Strategic Cap Table Additions: Promoters often use secondary sales to bring in specific, value-add new investors. A ROFR allows existing investors to block these hand-picked partners by purchasing the shares themselves.

- Deters Buyers and Causes Delays: Outside buyers are reluctant to spend weeks on due diligence if an incumbent can snatch the deal at the last second. This friction and the resulting 30-to-90-day delays often cause potential buyers to walk away entirely.

Say the ROFR terms are standard: 30 days to exercise the right (say yes/no to matching the offer), then 60 days to actually complete the purchase once exercised.

Now imagine the ROFR holder exercises the right – says yes, we’ll match this offer – but then, for whatever reason (funding constraints, a change of mind, an internal approval that falls through), doesn’t complete the purchase within those 60 days.

The selling shareholder has now lost 90 days – the full 30+60, during which their original third-party buyer’s offer has very likely gone cold and the seller is now back to square one.

The balancing act

At Auxano, we believe that managing a ROFR successfully comes down to balancing both parties’ perspectives through clear drafting to eliminate ambiguity.

Including mutually agreeable timelines could be one way to avoid protracted administrative delays and maintain the momentum necessary for successful secondary sales, thereby protecting the stakeholders’ interests.

Author,

Mansi Handa