In the previous blog, we looked at Conditions Precedent (CP) as the layer between signing the Share Subscription Agreement (SSA) and fund flow.

CPs must be completed before funds are remitted, even though the SSA has already been signed.

We had broadly classified CPs into:

- Regulatory and compliance

- Due diligence (DD) related

This blog focuses on DD-related CPs.

DD-Related CPs: Two Buckets

- Common and Standard CPs

These are recurring across most institutional transactions. Founders, particularly those who have raised capital before, are expected to anticipate them.

Typical examples include:

- Creation or expansion of an ESOP pool

- Finalisation of founder and key employee employment agreements

- Obtaining ISIN for de-mat issuance

- Basic cap table alignment and documentation

- Putting basic governance processes in place.

These are predictable in nature. When they appear as CPs, they are usually items that could have been addressed earlier.

- Transaction-Specific CPs (DD Findings)

These arise from diligence and are specific to the company’s history and structure.

Typical examples include:

- Renewal or formalisation of a significant customer or vendor contract

- Closure of inter-company loans or director loans outstanding on the books

- Repayment of related party exposures

- Situations involving co-founder equity where a departing founder’s shares were not formally bought back, requiring resolution before closing

- Board reconstitution is another common item, and where applicable, an independent director.

Other examples include the regularisation of past share issuances where allotments were made without proper RoC filings or board resolutions, and resolving gaps in intellectual property ownership or transfer to the company.

In regulated businesses, it may be necessary to obtain a no-objection or consent from a government authority where the company operates under a licence or concession. Similarly, consent from an existing lender may be required under financing arrangements, which is more typical in transactions involving larger cheque sizes.

These items are less predictable, but once identified, they tend to determine timelines.

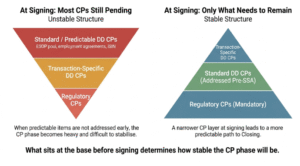

Where Delays Typically Arise

Regulatory CPs are largely procedural and follow defined processes and timelines.

At Auxano, our experience has been that execution challenges are more commonly seen within DD-related CPs, particularly the standard ones.

As discussed above, employment agreements are routinely expected in most transactions. The creation of an ESOP pool is also a standard requirement at the time of an institutional round. De-mat readiness, including obtaining ISIN, has effectively become a baseline expectation.

When these items come up during the CP phase, they point to areas that could have been addressed earlier.

For founders who have already been through a funding cycle, the expectation is that these elements are already in place.

Why This Matters

The nature of the CP list affects more than just timelines.

A larger and more complex CP list increases the number of dependencies before Closing. It also influences investor comfort, as overall legal and compliance hygiene is often seen as a reflection of operating discipline. In addition, it makes the process more iterative during the CP phase.

Closing Thought

CPs are intended to enable Closing.

When standard items form part of that list, the process shifts from execution to clean-up.

The difference between a smooth Closing and a delayed one is often set before the SSA is signed.

Author,

Mansi Handa