Statements like

“We are Founder friendly investors”,

“We close the investment in X hours”,

“Our data room checklist is short and concise”,

Are they really in favour of the founders or just trying to avoid the time, effort, resources and expertise required to conduct a thorough due diligence!!!

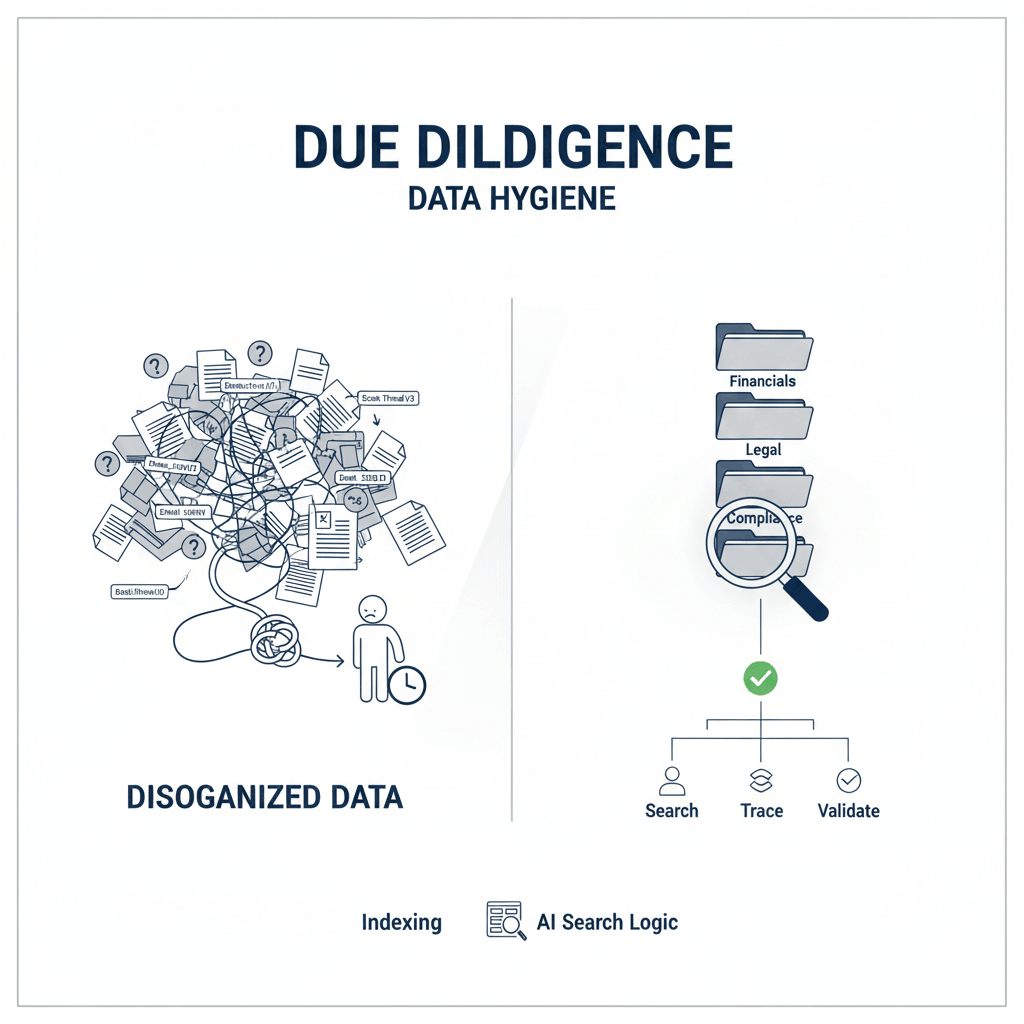

Experience: While going through the due diligence report conducted by an investor, I realised what we at Auxano call the similar documents an ‘Investor Note’ while many use it as a Due Diligence report.

Thought: Is neglect towards these finer details responsible for the start-up investing being viewed as a risky asset class in general???

Premise: One who does minimal background check before investing their/their investor’s money, how does one expect them to monitor the company on governance and compliance post investment???

Let’s begin by understanding, what goes in Due Diligence??

Due Diligence can have 6 sub-categories, namely:

- Legal Due Diligence

- Financial Due Diligence

- Regulatory Due Diligence

- Technical Due Diligence

- Business Due Diligence

- Founder Due Diligence

Most of the ecosystem stakeholders focus on Business Due Diligence, wherein they look at:

- User Growth

- Cohort Analysis

- Revenue No.

- App/website UI/UX

- TAM, SAM, SOM

- Problem statement

- Value Proposition

- Competitor Analysis

- Financial Projections

- Team Strength

The reports are more like restructured pitch decks.

Is this really Due Diligence???

In continuation to the structure of Due Diligence iterated above, let’s see what all must be covered under the various sub-categories:

1. Legal Due Diligence: This segment covers reviewing for any past/ongoing litigation on the company and validating the long term and short-term contracts that the company has entered into with its stakeholders, namely,

- Customers

- Suppliers

- Employees

- Investors

- Lessors

- And other vendors providing services to the company.

Reviewing does not conclude at having just seen the agreements, minute details must be considered and appropriate discussions around impact and mitigation must be discussed with the founders. The details include but are not limited to:

- Validity of the agreement

- Scope of work

- Cost and escalation provisions

- Governing laws

- Registration of the agreement and payment of stamp duty

- Provisions for termination

- Indemnification

- Non-Compete & Non-Solicit

- Confidentiality

- Representations and Warranties

Long term and short-term impact of each of these clauses across agreements must be evaluated.

2. Financial Due Diligence: Financial Due Diligence covers reviewing, validating the financial health and position of the company and rectifying the short comings. The documents that need to be validated include the following:

- Corporate Taxes: GST Returns, IT Returns, TDS Returns, Professional Tax Returns

- Tax Payments and Demand/Refund

- Audit Reports

- Books of Accounts

- Capitalization Policy

- Debtor & Creditor Ageing

- Asset & Liability Schedule

- Share Capital Recognition

- Details of Loans, Advance or Guarantees provided by the company

- Related Party Transactions

- Statutory payments like EPF and ESI

The documents must not be viewed in silos, the data from various sources must be cross checked and validated to ensure the internal reporting, external reporting and 3rd party reporting sync to reflect the same health.

3. Regulatory Due Diligence: This part of the due diligence includes validating the compliance under the MCA and Companies Act. These include:

- Registration & Licenses — PAN, TAN, GST, Start-up India, MSME, IEC, ESI, PF, Trade License, S&E License, Certificate of Incorporation

- Charter Documents — MOA & AOA, along with subsequent alterations

- Regulatory Filings — MGT 7, MGT 14, PAS 3/4/5, SH 7, AOC and others

- ESOP Policy

- POSH Policy

- Payroll Registers

- Statutory Registers

- Board Meeting and EGM — Notice, Minutes, Attendance

- RBI & FEMA compliances in case of foreign investment

4. Technical Diligence: This includes validating the tech stack, mainframe architecture and its scalability. Investors would want to look deeper into source code and training data but typically founder are not willing to share these details. Investors can use simpler methods of using the product anonymously and then requesting the usage and other data for the same account from the founder. Another lesser reviewed aspect of tech diligence includes optimisation of 3rd party services like cloud. Start-ups receive credits at the early stage from the providers and as the credits get exhausted, cloud charges constitute a large part of the operational spend. With the exit barrier, this hampers the growth of the company, thus at the outset a brief diligence on the optimisation must be considered.

5. Business Diligence: Besides the list shared in the earlier part, Intellectual Property registrations form a critical part of the Business Diligence

6. Founder Diligence — This includes checking the credit history of the founder, reference check from college/professional colleagues. An important constituent here is to check the legal history of the founder, if there have been any litigations, acquisitions, judgement or investigation on the founder for professional or personal reasons.

These minute details are many a times ignored by the investors and hidden behind the veil of ‘founder friendly investor’, but one must remember — ‘Investing is not a one-night stand, it’s a marriage’.

By not undertaking the detailed diligence, investors tend to harm themselves, their investors, peer investors, company and its stakeholders like employees, customers and suppliers.

Most importantly what also gets impacted is the entire ecosystem.

As some of the cases of misdoings unfold a ripple of events wherein diligent founder find it challenging to raise capital and investors take a hit on their conviction towards the asset class.

Auxano Approach: At Auxano we engage professionals and subject matter experts for the Due Diligence. These are conducted by 3rd parties to ensure objectivity and eliminate biases. We have a 108-point checklist at the onset of the due diligence which is followed up by queries and additional requirements as per the findings, nature of business and individual company.

Conclusion: Due Diligence is a pre-emptive measure. It does not ensure that the non-compliance would not occur but enables an investor to identify and ask the founders to deploy course correction measures.

Having known the shortfalls, an investor would be able to take better decisions. This would not only protect the capital but also increase the returns (may also defy the so-called ‘Power Law in VCs’).

Due Diligence is not a one time activity, there are follow-on actions to ensure long term impact of the efforts:

- Continued Monitoring through MIS

- Conducting detailed Due Diligence every 18–24 months or as maybe required.

Venture Capital in India is at its nascent stages, many practices are yet to evolve, and the regulators, professionals and investors have to work together to enable this ecosystem evolve while ensuring good practices.

From a Founder’s perspective also, Due Diligence is beneficial as:

- It enables the company to identify the areas where they lag.

- It enables the founders to identify the teams which lack competency.

- It enables the company to make robust systems, checks and balances and be prepared for the following rounds of fundraise.

- Avoid regulatory scrutiny and penalties.

- Lastly, acts as a risk mitigator for the founder as in case of any negative instance, the founder is protected as the investors had conducted their due diligence prior to investing.

The process involves time, money and efforts but is crucial as the ecosystem grows to ensure trust amongst the ecosystem stakeholders and prosperity of all.

Author (s):

Karan Gupta